Thailand’s tire market has clear growth momentum, even as trade friction rises. Mordor Intelligence estimates the Thailand tire market at USD 3.62 billion in 2025 and projects USD 4.81 billion by 2030, implying a 5.83% CAGR for 2025–2030. Another Thailand-focused forecast values the market at USD 3.51 billion in 2024 and expects USD 5.04 billion by 2030, with a 6.23% CAGR. Across both views, the direction is similar: demand is supported by vehicle production, exports, and a resilient replacement cycle, while cost and regulation remain persistent constraints.

Export conditions are more volatile. A Thailand export-focused source reports that exports reached 2.6 million units in the first seven months of 2025, down 24.4% year-on-year, after growth from 2020 to 2022 and a gradual decline afterward. It attributes the drop mainly to Thai products being subject to higher import tariffs than competitors, and it also highlights high anti-dumping duties imposed by the United States on large truck tires imported from Thailand. Separately, a global tire market report notes that in early 2025 the U.S. government imposed 25% tariffs on imported automobiles and components, including tires, under Section 232 and related trade authorities. Together, these points frame the near-term challenge: defending competitiveness when landed costs rise.

Where Growth Is Coming From: Aftermarket Strength and EV Pull

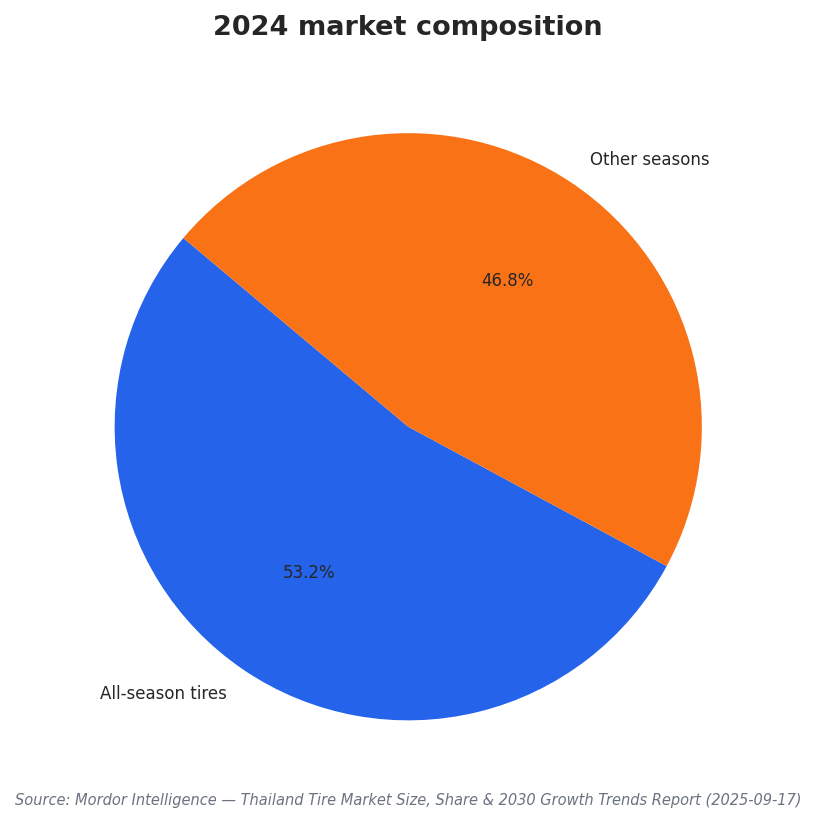

Domestic demand signals help explain why manufacturers keep investing despite tariff pressure. By end user, the aftermarket held 63.47% of Thailand’s tire market share in 2024, according to Mordor Intelligence, indicating replacement demand remains the anchor. By design, radial technology led with an 87.65% share in 2024, reinforcing how mainstream radial output is in Thailand’s product mix. By season, all-season tires captured 53.24% share in 2024. These segments create scale, but growth opportunities also come from newer requirements such as higher specifications and compliance-driven labeling, which the same source links to premium radial technology and EV-specific tire needs.

Policy-driven electrification is a specific pull factor for new tire specifications. Mordor Intelligence cites Thailand’s EV 3.5 policy, which provides THB 50,000–100,000 purchase subsidies and cuts excise tax to a minimum. It also points to a projected two-fifths jump in EV registrations during 2025, alongside a domestic-assembly rule requiring multiple vehicles built domestically for every imported unit by December 2026. Within the market breakdown, internal combustion vehicles still held an 86.71% share in 2024, but battery-electric cars are forecast to post the fastest segment CAGR at 5.88% through 2030. This mix suggests tire makers must support today’s dominant volumes while preparing for faster EV-led growth.

Capacity expansion is not only a Thailand story, but it directly affects the country’s supply chain strategy. IndexBox notes that expanding tire manufacturing capacity in Southeast Asia—particularly Vietnam, Thailand, and Indonesia—is creating demand for local compound mixing and material processing capacity. The same source adds that tariff treatment varies by trade agreement: natural rubber enters most Asian markets duty-free or at low rates of 0–5%, while synthetic rubber and carbon black face tariffs of 5–15% depending on origin and bilateral trade pacts. Meanwhile, a global rubber tire market report states Asia Pacific produced about 12.64 million tons of natural rubber in 2018 and says Thailand holds 33.4% of global natural rubber market share. For manufacturers, these inputs and tariff structures shape how they balance export pricing pressure with deeper localization and materials planning.

What is the outlook for Thailand’s tire market through 2030?

What export signal shows tariff pressure on Thai tire shipments in 2025?

How does EV policy influence product requirements for Thailand’s tire makers?

Which segments dominate demand inside the Thailand tire market?

What are the key pressures shaping Thailand’s tire manufacturing industry right now?