Thailand’s property market has been described as cautious in early 2026, yet the top end is moving in the opposite direction as branded residences expand across Bangkok, Phuket and resort destinations. The appeal is tied to lifestyle and to structure: buyers are not just purchasing a home, but a managed asset that combines services, security and brand association. CBRE Thailand said Bangkok’s overall condominium market had a slow start to 2026, with only 12 new project launches in the first quarter, as buyers took longer to make decisions amid geopolitical risks, a weak local economy and elevated oil prices.

Despite that slower broader backdrop, luxury performance in prime Bangkok locations held up. CBRE reported that completed luxury condominium projects recorded a 95% sales rate in the first quarter of 2026, while completed super-luxury projects recorded 86%. The pipeline told a similar story, with sales rates of 72% for luxury and 82% for super-luxury projects. This “two-speed” environment is shaping how developers position premium homes, with buyers increasingly looking for hospitality-standard management, private owner benefits, and rental flexibility alongside the core real estate proposition.

Why Thailand Leads Asia’s Branded Supply

C9 Hotelworks’ Asia Branded Residences Market Review 2026 shows the scale of the shift. It valued the Thailand branded residences market at THB205.3 billion (USD6.4 billion) in 2026, up 13.3% year on year, with 13,124 launched units. Thailand now accounts for 26% of Asia’s launched branded residence supply, the highest country share in the region. Asia Property Awards also cited total Thai supply at 63 properties and 13,947 units, while noting that Asia’s branded residences sector reached THB1.3 trillion across 50,025 launched units, up 30.3% year on year.

The same report highlights how Thailand’s growth is split across urban and resort markets. Bangkok remains the largest urban branded residences market, with 5,031 units. Phuket has 3,465 units and leads Asia’s resort segment by unit count, according to Asia Property Awards. Beyond the biggest destinations, the pipeline is also broadening. Koh Samui is described as an emerging branded villa market, with its luxury holiday villa sector reaching 3,055 properties in 2025, up 37% year on year. The takeaway for buyers is choice across formats and locations, while developers compete on the operating platform and post-handover experience.

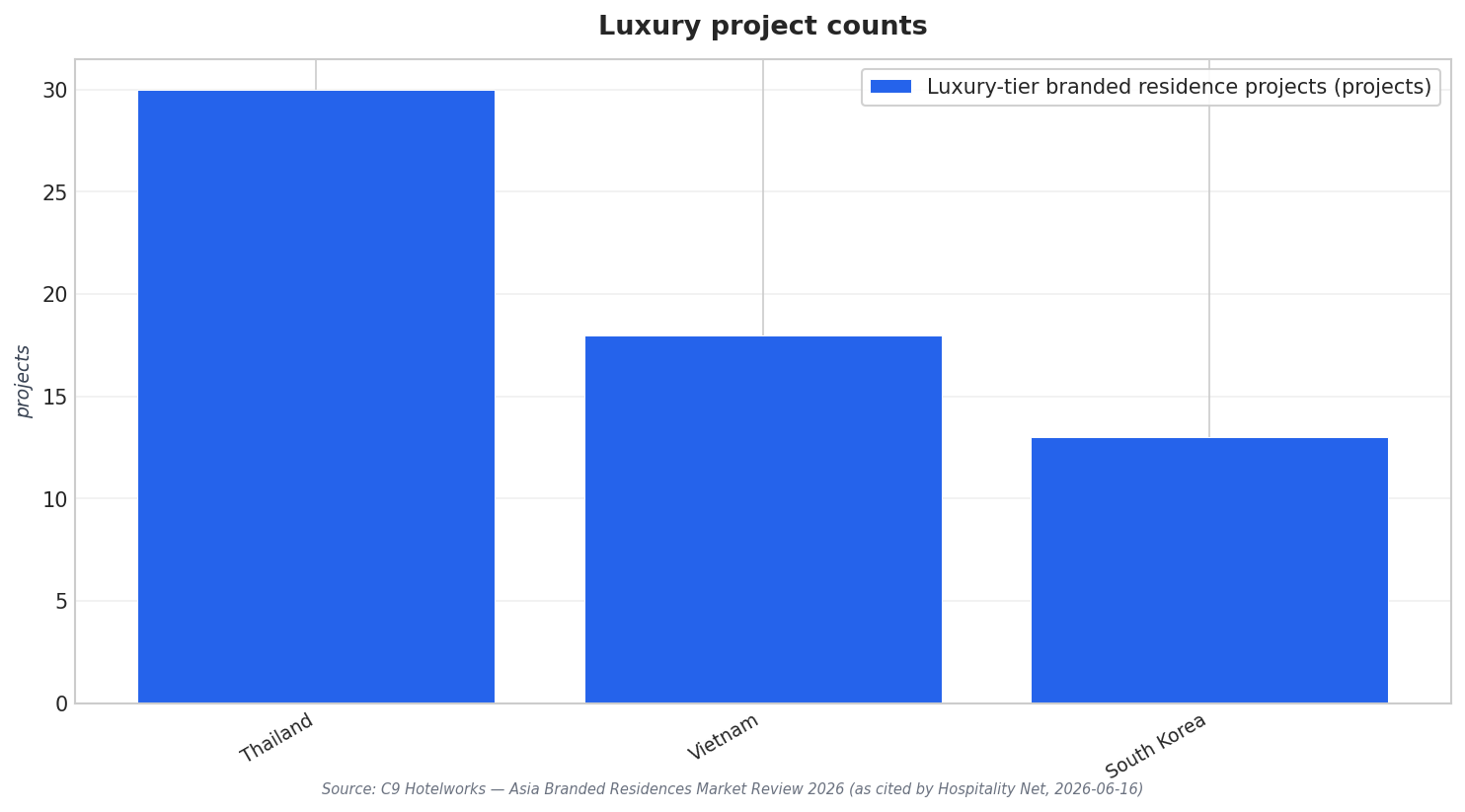

Competition is also intensifying at the luxury tier across Asia. C9 Hotelworks data, cited by multiple outlets, says Vietnam leads the region by aggregate market value, while Thailand moved to the forefront of the luxury segment with 30 luxury-tier branded residence projects, ahead of Vietnam (18) and South Korea (13). Bangkok Post adds that in Thailand, “luxury” refers to units priced at least 20 million baht, and villas priced at least 100 million baht. As land and construction costs rise, the same report notes developers pivoting toward branded residences or combined hotel-residence models to pursue stronger returns than standalone hotels.

How large is Thailand’s branded residences market in 2026?

What share of Asia’s launched branded residence supply does Thailand hold?

Which Thai locations lead branded residence unit counts?

How is the luxury end performing in Bangkok compared with the broader condo market?

What is driving the shift in the Thailand branded residences market toward a safe-haven narrative?