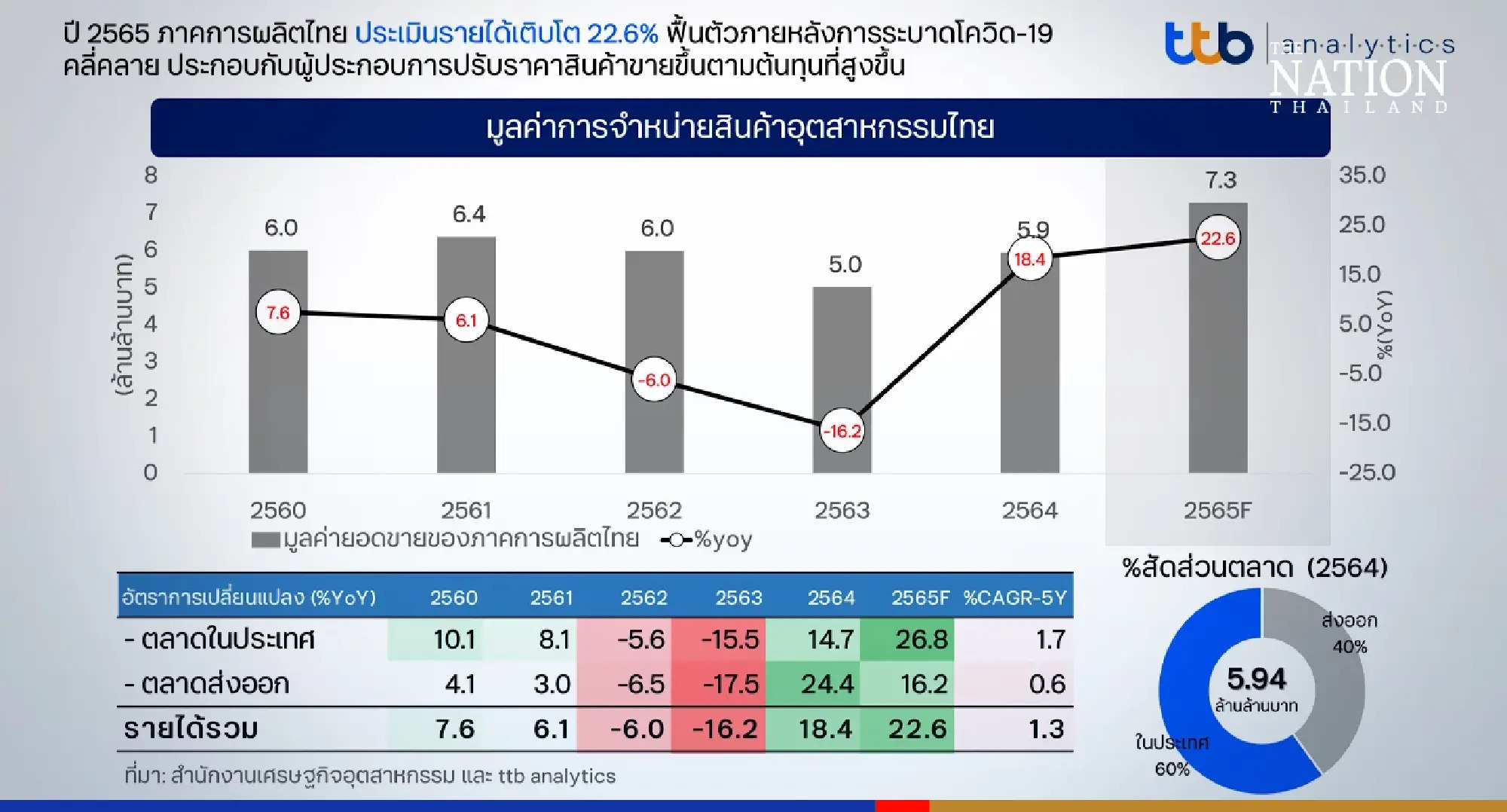

Thailand’s industrial sector faced another difficult month in August 2025 as Thailand Factory Output Decline dropped 4.19% year-on-year, a sharper fall than the expected 2.1%. The result highlights continued challenges for Southeast Asia’s second-largest economy as weak global demand, strong currency pressures, and domestic cost burdens weigh on production.

Thailand Factory Output Decline Weakens Beyond Expectations

The Manufacturing Production Index (MPI) contracted 4.19% year-on-year and 2.1% month-on-month in August. This follows a 3.75% drop in July, marking the second consecutive month of worsening industrial conditions. The steeper-than-expected decline signals that Thailand’s recovery momentum is faltering, with factories scaling back operations amid sluggish domestic and international orders.

Officials from the Industry Ministry noted that temporary factory closures for relocation and maintenance also contributed to the short-term decline. However, the broader trend points to deeper structural pressures—such as high inventory levels and weak export growth—that have persisted throughout 2025.

Automotive and Petroleum Lead the Contraction

The Thailand Factory Output Decline was driven primarily by weak performance in key sectors like automotive manufacturing and petroleum refining.

Automobile output fell 8.09% year-on-year, compared with a 7.66% drop in July, reflecting slower global car demand and a slump in vehicle exports. Petroleum refining declined 7.98%, an improvement from -18.43% previously, but still a major drag on industrial performance.

Read Also: The Strategic Integration of EV Shuttle Routes into Bangkok’s Mass Transit

The food and beverage sector, another major contributor to Thailand’s manufacturing base, also posted declines due to lower domestic consumption and weak exports. These sectors collectively represent a large portion of Thailand’s industrial activity, making their downturn particularly impactful.

Pockets of Growth Offer Limited Relief

Despite the broad downturn, certain industries managed to grow. The Ministry of Industry reported output gains in clothing and apparel (+12.74%), electronic components (+8.43%), and basic iron and steel (+7.72%).

These improvements suggest that Thailand is still maintaining competitiveness in niche export segments like electronics and intermediate goods, supported by foreign investment and regional supply chain integration. However, these gains are too limited to offset the steep declines in heavier industries such as automotive and energy, which continue to weigh on the overall index.

Weaker Exports and Global Pressures Intensify

Thailand’s export-driven economy remains highly sensitive to global demand fluctuations. The recent slowdown in exports, combined with U.S. trade policy uncertainty, has created additional headwinds. A strong baht currency has also made Thai exports less competitive, while falling tourist arrivals have weakened domestic consumption—a secondary demand driver for manufactured goods.

These pressures have prompted the Industry Ministry to revise its industrial growth forecast for 2025 down to just 0%–1%, a significant downgrade from earlier expectations. Officials cited elevated household debt and global trade instability as key risks limiting industrial recovery over the next year.

Economic Implications of the Factory Output Decline

The sustained Thailand Factory Output Decline poses challenges for broader economic stability. Manufacturing accounts for a substantial share of Thailand’s GDP, and prolonged weakness in this sector could slow job creation and investment inflows.

Export competitiveness is also at risk as other regional players—like Vietnam and Indonesia—continue to expand their industrial bases and attract new manufacturing projects. Thailand’s policy focus will likely need to shift toward industrial diversification, technological upgrading, and easing financial pressures on small and medium-sized manufacturers to stabilize output in 2026.

Read Also: EEC Thailand 2025 Redefines Future Supply Chains

Thailand Factory Output Decline: Navigating a Fragile Recovery

While certain bright spots in electronics and apparel show resilience, Thailand’s industrial growth outlook remains fragile. Without a rebound in global trade and export orders, factory utilization rates are expected to stay low through early 2026.

Government efforts to boost domestic demand, attract new investment, and support supply chain modernization will be critical to reversing this trend. Addressing the structural issues behind the Thailand Factory Output Decline will determine whether the sector can regain momentum and sustain growth in the coming year.